Commercial auto insurers are now looking beyond fleets’ five-year loss histories when the time comes for renewals, expecting to see how fleets use telematics data to improve driver behavior, coach employees and reduce risk over time.

Panelists at the Samsara Beyond conference in Las Vegas argued last week that fleets gain the greatest value from connected fleet technology when it becomes more than a compliance tool. Driver scorecards, coaching records, AI-detected events and video can all be used to demonstrate a strong safety culture, identify operational risks and strengthen their position during insurance renewals negotiations.

“It’s not an individual data point that we’re looking for,” said Hobie Bond, head of telematics and IoT at Zurich North America. “It’s really a collection of data points, and perhaps more importantly, how are those data points trending over time?”

Improvement matters more than perfection

While loss records remain important, Bond said they no longer tell the complete story. Instead of focusing on individual events like harsh braking events or distracted-driving alerts, underwriters look for patterns and whether those are improving over time.

“We really want to understand something more than just simply yes/no,” Bond said. “We want to understand effectiveness. And the greatest way to understand effectiveness, of course, is to see changes in the score over time, preferably on an improving basis.”

But the timing also matters, he added. A carrier that implemented cameras and coaching only six or nine months ago may still have loss trends that reflect years of operating without those tools. Looking only at historical claims without considering recent behavioral improvements can lead to a distorted, incomplete picture of risk.

“Commercial auto [has] problems, it’s not made money collectively in roughly 15 years, so there’s a lot of pressure on the underwriter to get the right rates on the accounts, and we want to be able to differentiate accounts appropriately based on how telematics is being used and how effectively it’s being used within the fleet,” he said.

Martin Sullivan, practice leader at Acrisure, agreed with Bond, but also added that fleet executives should reevaluate their safety data and start seeing it as a strategic asset that they should care about even when insurance isn’t involved.

“What shows up on the loss runs is a fraction of the total impact – reputation, ability to get new contracts, driver morale. Safety data is a window into the fuller picture.”

Sullivan also challenged the idea that compliance and safety are interchangeable. “Compliance and safety are barely related. Being compliant is important, but it doesn’t make you safer,” he said, explaining that insurers want to see evidence of a fleet’s safety culture through leading indicators such as coaching activity, driver improvement trends and how management responds when incidents occur, not loss runs and P&L statements,

“The data doesn’t lie,” Sullivan said. “You’re going to show constant improvement if you guys are coaching drivers and actually disciplining drivers and looking at your routes.”

He added that being able to show that kind of improvement can also open the door to alternative insurance options, including captives and self-insurance, giving fleets more control over their insurance costs.

Use telematics data to make decisions

Building that kind of safety culture, however, requires fleets to make sense of the data they collect and use it to make decisions.

Lisa Paul, executive vice president of Alliant Insurance Brokerage, said leading crash indicators are valuable when they’re connected to claims and operational data, allowing fleets to identify patterns that wouldn’t be obvious from loss history alone.

“We had a customer that we operationally sat down and looked at everything,” she shared an example with the audience. “Lo and behold, everything over 250 miles was just trouble for them.”

Although those long-haul moves represented only about 4% of the company’s revenue, they generated a disproportionate share of its losses.

“It made sense for them to get rid of the units and the drivers of the over 250 [miles], find a different partner to do that work for them and really focus their revenue on the short-haul portion of their business far more profitably,” Paul said, noting that such conversations and evaluations shouldn’t happen only at the renewal time.

Instead, brokers should be reviewing telematics and claims data with fleets months before policies expire, examining which routes, vehicles and operations are driving losses and whether operational changes could improve both profitability and insurability.

“Our goal is to not only take the data but also to make operational strategy and success so the CFOs and the business owners can really take a look, price their transportation services better…based on today’s drivers, today’s customers, and today’s shippers, so that we can make strategic conversations,” Paul said.

Video keeps paying dividends

The panel also spoke about how much cameras improve claims outcomes or wipe away the claim altogether.

Bond described one case in California where a pedestrian intentionally threw a bicycle into a commercial vehicle before falling to the ground in a staged collision. The truck driver was initially arrested for a hit-and-run. The video footage later proved the incident had been staged, leading to the driver’s exoneration and release.

Paul shared another example involving a large aggregate hauler in Hawaii. Just 10 days after installing inward- and outward-facing cameras, another motorist alleged the fleet’s driver had struck their vehicle and injured three people.

“The claim adjuster was able to pull up the video and wiped away the claim,” Paul recalled, adding that the incident has also changed the driver’s perception of cameras – previously, he was one of the most vocal to protest them. The driver later wrote to the company’s safety department, “I’m sorry, I was wrong. This clearly showed that I am still the great driver you always knew me to be.”

Paul also cited results from Alliant’s own large transportation fleets using Samsara-connected cameras, saying they saw exoneration rates approaching 28%, exceeding the 18% to 22% rates reported in earlier American Transportation Research Institute research.

True cost of collisions

Bond added that commercial auto insurance now accounts for a much larger share of a fleet’s overall insurance costs than it did a decade ago. About 10 years ago, commercial auto typically represented roughly 15% of a fleet’s insurance package. Today, it is approaching 25%.

This is why crashes involving commercial vehicles can trigger workers’ compensation claims when drivers are injured, and those claims tend to be much more severe than the average workplace injury.

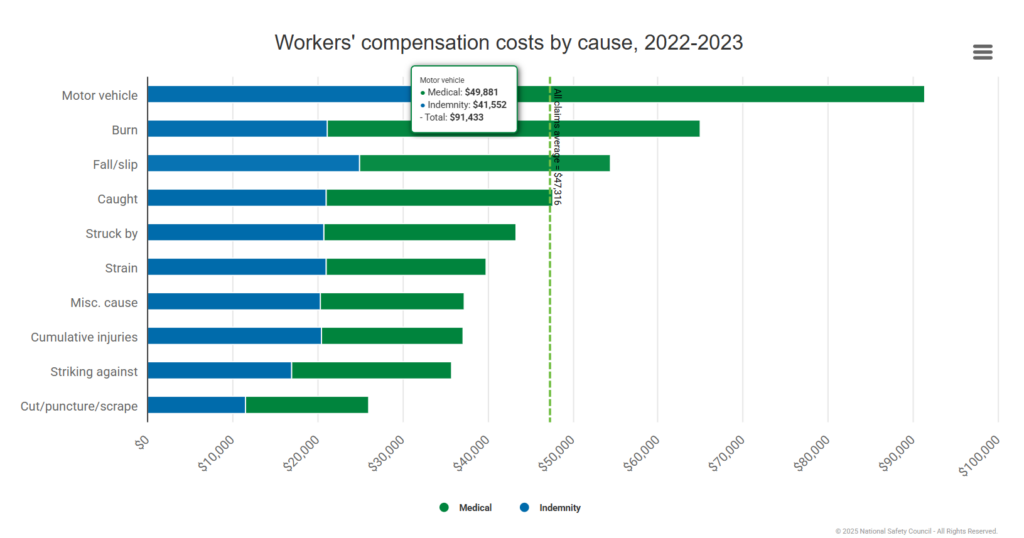

“When there is a motor vehicle accident and one of your drivers is involved, if there is a work compensation claim that comes along with that, that work compensation claim is on average two and a half times more severe,” he said. According to most recent National Council on Compensation Insurance’s data, the most costly lost-time workers’ compensation claims by cause of injury in the U.S. result from motor-vehicle crashes, averaging $91,433 per claim.

As a result, reducing crashes through driver coaching, telematics and safety technology can improve performance across several insurance lines, not just commercial auto. Instead of looking only at premium reductions, fleets should also consider the broader “total cost of risk,” Bond said, which includes vehicle damage, workers’ compensation, legal expenses, downtime and other indirect costs associated with collisions.

Credit: Source link