Tightening capacity continues to push rates higher.

That’s the latest take from DAT Freight & Analytics. The trucking industry research firm has found that truckload spot rates rose significantly faster than freight volumes in June.

This trend, DAT analysts said, signals that tightening truck capacity — rather than surging freight demand — is driving the current freight market.

DAT’s June Truckload Volume Index (TVI) report found that while freight volumes posted modest month-over-month gains, pricing continued to accelerate across all major trailer segments.

Most notably, the national average dry van spot rate climbed above the contract rate for the first time since February 2022, a milestone that underscores the market’s changing dynamics.

According to DAT, June’s TVI showed:

- Dry van: 262, up 11% from May and essentially unchanged from June 2025.

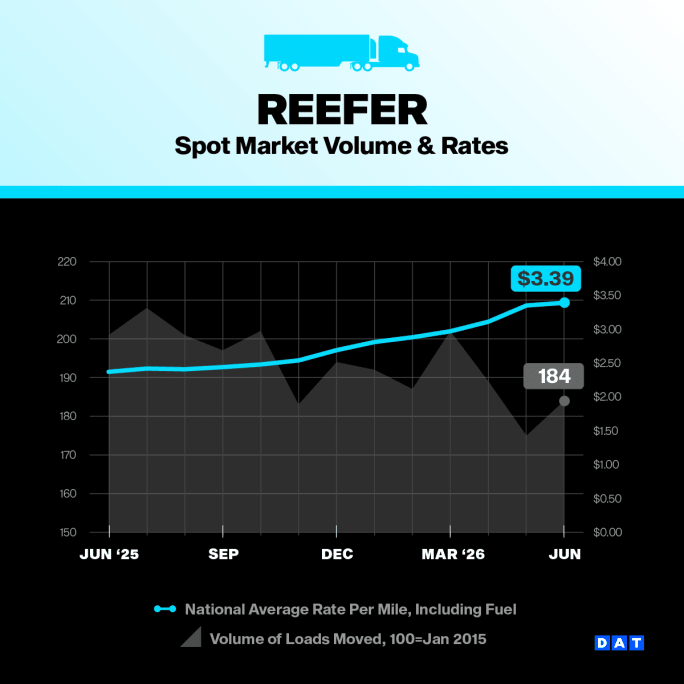

- Refrigerated: 184, up 5% from May but down 8% year over year.

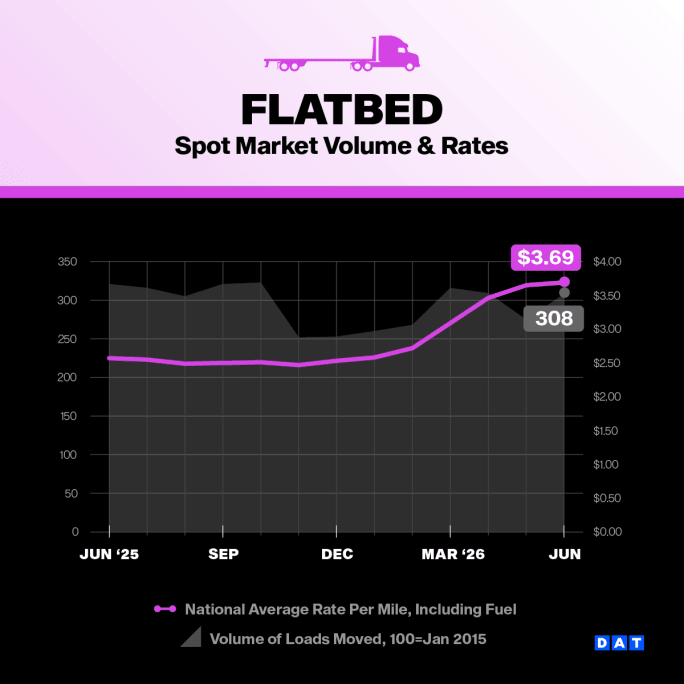

- Flatbed: 308, up 12% from May but down 4% from June 2025.

Despite relatively flat annual freight volumes, linehaul rates jumped at least 39% year over year across all three trailer types.

DAT attributed much of the tightening capacity to ongoing regulatory changes and immigration enforcement that have reduced the pool of qualified truck drivers.

Flatbed Rates Reach New Record

National average spot rates increased across every equipment category during June.

Dry van spot rates averaged $3.00 per mile, an 11-cent increase from May. Refrigerated freight averaged $3.39 per mile, up 4 cents, while flatbed spot rates climbed to $3.69 per mile, also up 4 cents and establishing a new all-time high.

Flatbed spot rates climbed to $3.69 per mile in June.

DAT Freight & Analytics

After removing fuel surcharge effects, linehaul pricing strengthened even more dramatically:

- Dry van: $2.37 per mile, up 21 cents.

- Reefer: $2.70 per mile, up 14 cents.

- Flatbed: $2.94 per mile, up 16 cents and another record.

Compared to June 2025, van linehaul rates increased 45%, refrigerated rates rose 39%, and flatbed rates climbed 40%. DAT said those were the largest year-over-year percentage gains since mid-2021.

Contract Rates Continue to Lag

Contract pricing showed more modest movement.

Average all-in contract rates slipped slightly for both van and refrigerated freight as declining fuel surcharges offset higher base rates. Van contract rates averaged $2.89 per mile, down 3 cents from May, while reefer contract rates fell 6 cents to $3.22 per mile.

Flatbed contract pricing bucked the trend, rising 3 cents to $3.80 per mile.

Contract linehaul rates continued to improve, however, increasing to $2.26 per mile for van freight, $2.53 for refrigerated freight and $3.05 for flatbed.

Spot-Contract Gap Signals Growing Carrier Leverage

The relationship between spot and contract pricing continues to shift in carriers’ favor, DAT said.

Dry van spot rates moved above contract pricing for the first time in more than four years. Refrigerated freight’s spot premium widened to 17 cents per mile from 7 cents in May.

Refrigerated freight averaged $3.39 per mile in June.

DAT Freight & Analytics

Flatbed remains the lone exception, with contract linehaul rates still exceeding spot pricing. However, that difference has narrowed considerably, falling to just 11 cents per mile in June compared to 52 cents a year earlier.

“The difference between spot and contract rates has narrowed steadily for more than a year, and carriers are gaining pricing power across the board,” said Dean Croke, DAT industry analyst. “Van spot beating contract for the first time in four years, and flatbed hitting an all-time high in the same month, shows real capacity pressure. If demand were driving this, volumes would be climbing too, and they’re not.”

The June report adds to growing evidence that the freight market recovery is being driven more by constrained trucking capacity than by robust freight demand, giving carriers increased leverage in pricing negotiations even as shipment volumes remain relatively subdued.

Credit: Source link