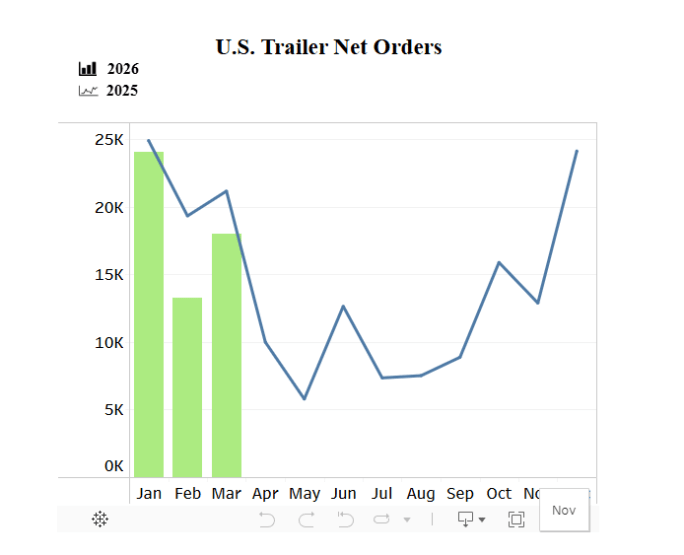

U.S. trailer demand came in stronger than expected in March. According to FTR, net orders rose 36% month over month to 18,045 units.

The increase runs counter to typical seasonality, which usually sees orders fall about 20% from February to March.

Even with the gain, orders were down 15% year over year and remained below the 10-year March average of 20,276 units.

For the current order season (September 2025 through March 2026), trailer orders are down 19% year over year and off 15% year to date.

Builds Rise but Reflect Ongoing Production Discipline

Trailer production also moved higher in March, with builds increasing 15% month over month to 17,501 units. However, output was still 1% below the same month last year, with year-to-date builds also trailing 2025 levels by 1%.

According to FTR, the data points to continued production discipline among manufacturers as they manage softer demand conditions.

FTR said that persistent headwinds continue to limit trailer demand, including elevated steel and aluminum costs, trade uncertainty and high financing costs.

FTR said the recent uptick in orders has not signaled a broader demand recovery. Instead, trailer purchases remain largely replacement driven as fleets continue to operate with excess trailer capacity.

At the same time, stronger Class 8 truck demand is drawing a greater share of fleet investment. Improving asset utilization, firmer rate expectations, and clearer pricing tied to tariffs and upcoming EPA 2027 NOx regulations are driving earlier-cycle truck orders.

Cost Pressures and Uncertainty Weigh on Outlook

FTR noted that persistent headwinds continue to limit trailer demand, including elevated steel and aluminum costs, trade uncertainty, high financing costs, and constrained capital spending.

Those factors are keeping orders relatively subdued despite improving freight conditions, leaving trailers a lower priority in fleet capital allocation decisions.

Credit: Source link