Spot market rates continued to trend upward in May but have cooled in the most recent week ended June 19.

The softening marked the end of a remarkable 24-week of consecutive rate increases for flatdeck haulers in the United States.

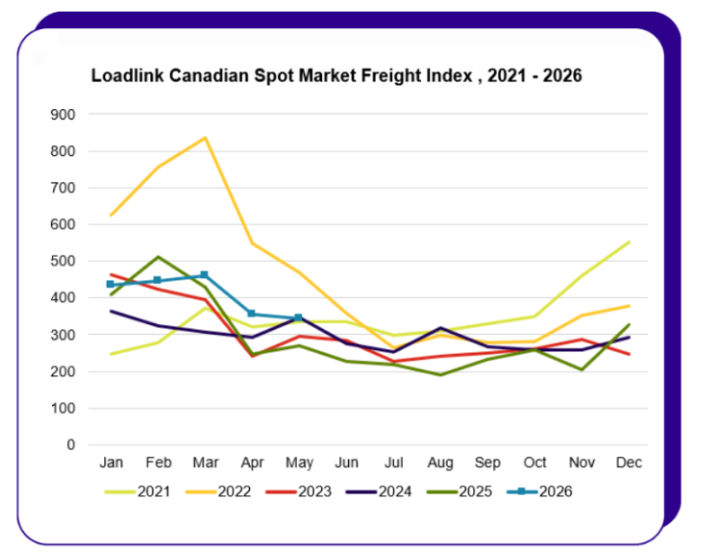

Canada’s spot market saw freight volumes well above year-ago levels in May, with loads to the United States more than doubling year over year, according to Loadlink.

Loadlink: Cross-border freight remains hot as outbound loads more than double

Canada’s spot freight market remained significantly stronger than a year ago in May, led by another surge in cross-border traffic, according to Loadlink.

Overall freight volumes were down 3% from April but remained 28% higher than May 2025. The biggest story was outbound freight to the U.S., which was up 109% year over year for the second consecutive month, despite a 22% decline from April’s elevated levels.

Cross-border freight accounted for 60% of all postings from Canadian-based customers. While outbound loads continued to drive growth, inbound freight from the U.S. showed signs of recovery, increasing 15% month over month after a weaker April. Inbound volumes remained 5% below year-ago levels.

Domestic freight also remained strong, with intra-Canada loads up 47% compared to May 2025, although volumes slipped 6% from April.

Capacity loosened slightly during the month, with the truck-to-load ratio rising to 1.96 trucks per load from 1.86 in April. However, the ratio remained 29% below May 2025 levels, indicating a much tighter market than a year ago.

“Two months in a row of outbound more than doubling is a real signal,” said James Reyes, general manager of Loadlink.

DAT: Spot rates climbed in May despite lower freight volumes

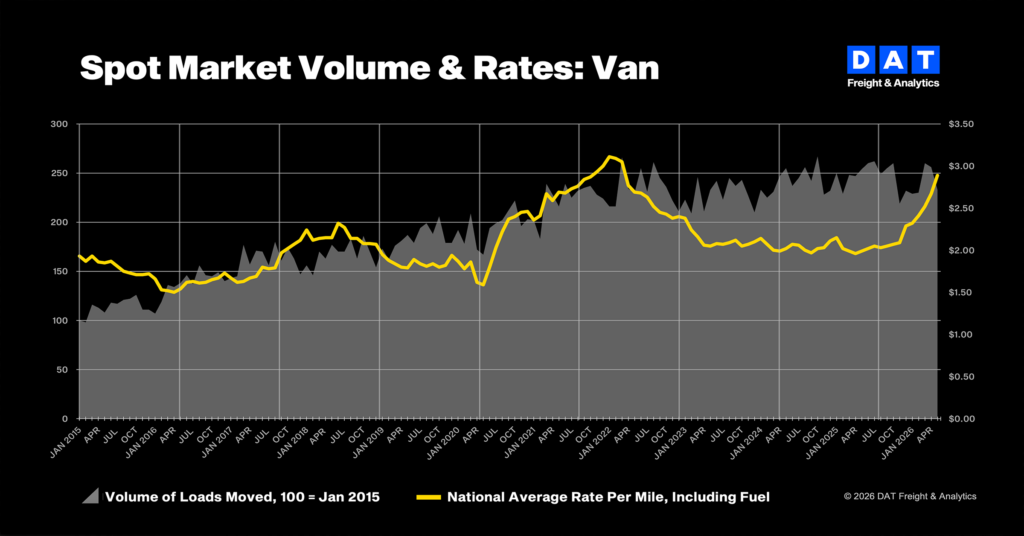

Truckload spot rates strengthened in May even as freight volumes declined, according to DAT Freight & Analytics, as tighter capacity outweighed softer demand.

DAT’s Truckload Volume Index fell across all major equipment types compared to April, with van volumes down 9%, refrigerated freight down 10%, and flatbed loads down 14%. Despite the decline, spot rates rose sharply, with van rates increasing 22 cents to $2.89 per mile, reefer rates climbing 24 cents to $3.35, and flatbed rates gaining 19 cents to $3.65.

DAT attributed the stronger pricing to capacity constraints driven by the CVSA International Roadcheck inspection blitz, the Memorial Day holiday, and ongoing immigration enforcement that continues to reduce the available driver pool. Truck-post data also showed some carriers parked equipment during Roadcheck week to avoid inspection-related delays.

The shift of capacity from spot to contract freight further tightened the market, as carriers sought the stability of fuel surcharge programs. That trend helped push reefer spot rates above contract rates in May, with reefer spot freight averaging $3.35 per mile compared to $3.28 on contract freight.

Year over year, spot rates remained dramatically higher, with van rates up 90 cents per mile, reefer rates up 99 cents, and flatbed rates up $1.07.

“Last month’s lower volumes do not mean May was a weak freight market,” said Dean Croke, principal industry analyst at DAT. “The capacity supply has come down to meet demand, and carriers in the spot market are being compensated for it.”

Contract rates also edged higher during the month, rising 6-7 cents per mile across all major equipment categories.

Spot market cools seasonally, remains far stronger than 2025

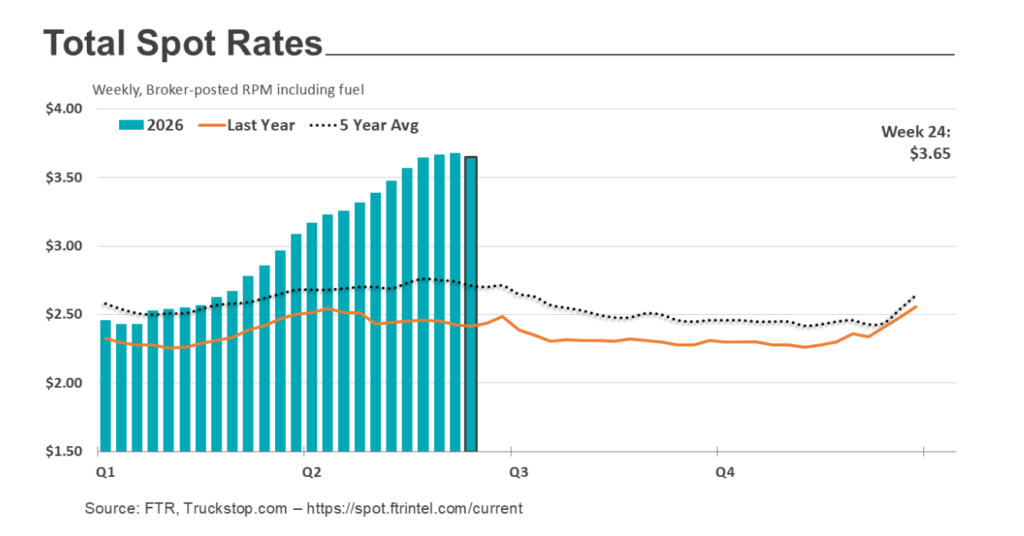

More recently, Truckstop.com and FTR Transportation Intelligence reported a modest seasonal slowdown in spot freight activity during the week ending June 19, but market conditions remain significantly stronger than a year ago.

The overall Market Demand Index (MDI) fell 20.9 points to 162.4 as load postings declined 7.7% and truck availability increased 4.2%. Spot rates slipped 0.6% to $3.65 per mile, ending a 21-week streak of weekly gains.

Despite the pullback, the market continues to outperform 2025. The overall MDI was up 96.7% year over year, while spot rates were 50.5% higher than the same week last year.

All major equipment segments saw demand ease. Flatbed’s MDI fell 28.6 points to 238.4, refrigerated dropped 62.9 points to 229.8, and dry van declined 13 points to 251.4. Flatbed spot rates also ended a 24-week streak of consecutive increases.

Analysts described the slowdown as a typical “mid-June slump” rather than a sign of weakening fundamentals. Van rates are expected to strengthen again heading into the July 4 holiday shipping period.

Meanwhile, diesel prices continued to fall, dropping 15 cents to $5.05 per gallon. Excluding fuel surcharges, spot rates for dry van and flatbed freight actually increased week over week, highlighting the strength of the underlying market even as all-in rates softened.

For the first time since early March, fuel-adjusted spot rates were slightly higher year over year than all-in rates, reflecting the sharp decline in diesel prices over the past several weeks.

Credit: Source link