Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

As we head into the halfway point of the year, the latest May and June data and analysis indicate that the recovery that began earlier this year is continuing, after nearly three years of freight recession.

Industry analysts say the rebound is being driven less by stronger freight demand and more by a shrinking supply of trucks and drivers. Those capacity constraints are finally giving carriers more pricing power, higher rates and more revenue.

Freight Volumes Slip But Rates Climb

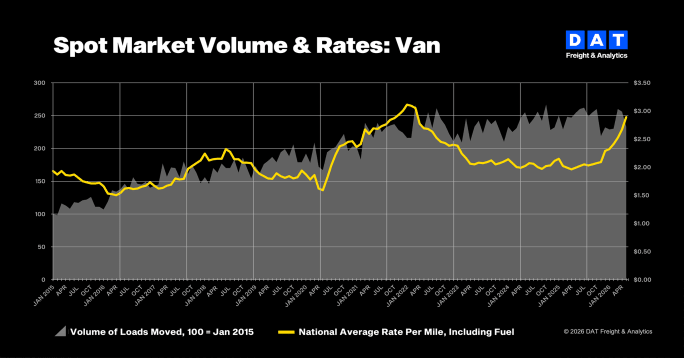

DAT Freight & Analytics’ May data showed that while truckload volumes fell month over month across van, refrigerated, and flatbed freight, spot rates increased in all three segments.

DAT reported van spot rates rose 22 cents per mile in May, while reefer rates increased 24 cents and flatbed rates gained 19 cents.

DAT’s Dean Croke said May’s spot market looks stronger than freight volume data alone would suggest.

DAT Freight & Analytics

“Last month’s lower volumes do not mean May was a weak freight market,” said Dean Croke, principal industry analyst at DAT.

“The capacity supply has come down to meet demand, and carriers in the spot market are being compensated for it.”

DAT attributed the tighter market to a combination of factors, including the CVSA International Roadcheck inspection blitz, Memorial Day disruptions, ongoing immigration enforcement, and carriers shifting equipment toward contract freight where fuel surcharge programs offer more predictable cost recovery.

The result was a spot market that appeared stronger than freight volume data alone would suggest, Croke said.

Capacity Constraints Continue to Tighten the Market

ACT Research sees the same trend continuing into June.

According to ACT, truckload spot rates, excluding fuel, are on pace to increase by more than 40% year over year this month.

“Tighter supply remains the main reason for accelerating rates,” said Tim Denoyer, vice president and senior analyst at ACT Research.

ACT pointed to several forces reducing available capacity, including lower equipment investment during the downturn, driver shortages, stricter regulatory enforcement, immigration policies, crackdowns on fraudulent electronic logging devices, and the closure of some driver training schools.

According to ACT, truckload spot rates, excluding fuel, are on pace to increase by more than 40% year over year this month.

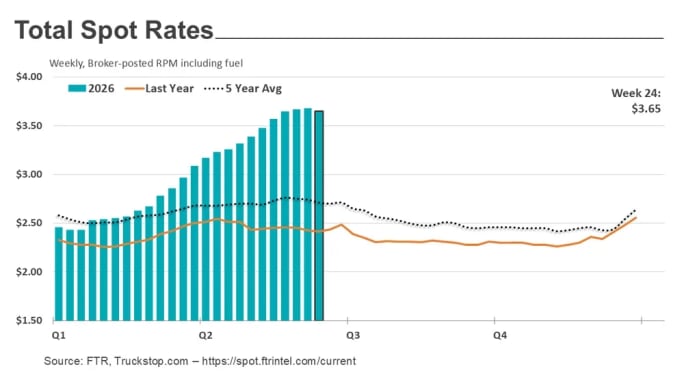

FTR and Truckstop.com

Driver Shortages, Enforcement Actions Reduce Capacity

ACT’s Driver Availability Index remained deep in shortage territory in May at 32.6, well below the neutral level of 50, although up slightly from April.

Ken Vieth, ACT president and senior analyst, said evidence suggests some drivers exited the market even before federal enforcement actions targeting non-domiciled CDL holders became official in March.

“A strong case can be made that the driver supply will remain tight for an extended period,” Vieth said.

Trucking Revenues Show Signs of Recovery

While capacity constraints have been the primary catalyst, demand indicators also have shown signs of improvement.

FTR reported first-quarter trucking revenues rose 4.3% year over year, with general freight revenues increasing 6.9% and long-distance general freight revenues climbing 6.5%.

Those gains suggest freight demand is improving from recessionary levels, though not enough on its own to explain the sharp increase in rates.

“The U.S. freight cycle has so far been supply-driven,” ACT noted, although improving industrial activity, tighter inventories, and easing tariff concerns could provide additional support for freight demand in the months ahead.

Spot Market Still Running Well Ahead of 2025

Recent data from Truckstop.com and FTR show the market remains considerably stronger than a year ago despite some expected seasonal cooling in mid-June.

For the week ending June 19, spot rates and demand eased modestly across van, reefer, and flatbed equipment, reflecting what analysts described as a typical “mid-June slump.”

However, conditions remained dramatically stronger than last year. Truckstop and FTR reported the Market Demand Index was nearly 97% higher year over year, while spot rates were up more than 50%.

Analysts said the recent decline in diesel prices has further improved carrier economics by boosting fuel-adjusted rates.

What to Expect

Most analysts expect some seasonal moderation after the July 4 holiday, but they do not foresee a return to the oversupplied conditions that defined much of the freight recession.

While higher rates could eventually attract additional drivers and equipment back into the market, ACT and DAT both suggest regulatory changes, enforcement actions, and ongoing driver availability challenges are likely to keep capacity constrained for the foreseeable future.

Credit: Source link