ATRI’s latest research points to litigation, social inflation, and soaring claims costs as key drivers behind record-high liability premiums for trucking fleets. But there are things motor carriers can do.

Trucking fleets are paying record-high liability insurance costs even as crash rates decline, according to new research from the American Transportation Research Institute.

ATRI’s latest insurance study found that average liability premiums climbed nearly 38% between 2015 and 2024, reaching 10.2 cents per mile. In ATRI’s annual industry issues survey, insurance ranked as trucking’s third-biggest concern in 2025, behind only the economy and lawsuit abuse.

Its May 2026 report examines the rising costs of commercial auto liability insurance in the trucking industry and how motor carriers can mitigate them.

Why Does Trucking Liability Insurance Cost So Much?

ATRI said insurance pricing is driven by a mix of crash trends, economic conditions, litigation, and what the industry calls “social inflation” — rising claim costs fueled partly by larger verdicts and more aggressive legal tactics.

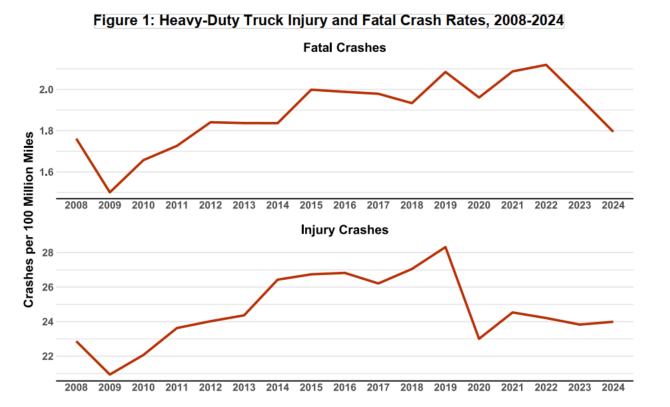

One of the report’s more striking findings: insurance costs continued climbing even as truck crash rates fell.

After the disruption caused by the pandemic, truck-involved crash rates have come down from their pre-pandemic high. ATRI also points out that “truck-involved” crashes most often are the fault of other vehicles, especially with the rise in distracted driving.

From 2021 through 2024, liability premium costs rose 18.6% to 10.2 cents per mile. During roughly the same period, heavy-duty truck crash rates dropped 2.6%, according to ATRI. Injury crash rates were down more than 15% from their 2019 peak, while fatal crash rates dropped nearly 14%.

But claim costs moved in the opposite direction. Fleets surveyed by ATRI reported a 33.1% increase in per-mile liability losses.

Smaller carriers were hit especially hard.

Fleets operating 5 to 25 trucks paid the highest per-mile premium costs in 2024 — nearly double the rate paid by fleets with 101 to 250 trucks. ATRI said those insurance costs consumed nearly 5% of total revenue for smaller operators.

The prevalence of plaintiff attorney billboards targeting trucking increases is a sign of the role of growing litigation expenses in the rising cost of claims,.

If Crash Rates Are Down, Why Are Insurance Premiums Up?

Commercial auto insurers, meanwhile, have spent most of the past decade paying out more in claims than they collect in premiums — a trend that continues to push rates higher.

Premium costs for excess coverage in particular rose at an even higher rate. From 2021 to 2024, per-mile premium costs for the $5 million to $10 million insurance layer rose by 34% to 1.58 cents per mile. Per-mile premium costs for the $10 million to $15 million layer rose by 45% to 1.05 cents.

These increases in excess coverage expenses point to the role of growing litigation expenses in the rising cost of claims, ATRI said.

Rising medical costs in general are also a factor, as well as “social inflation,” the increase in claim payouts and losses caused by social factors and societal attitudes.

ATRI pointed to several drivers behind “social inflation,” including nuclear verdicts, heavy attorney advertising, third-party litigation funding, and aggressive plaintiff strategies such as the “reptile theory.”

What Can Fleets Do to Reduce Insurance Costs?

Many insurance cost pressures are outside fleets’ control. For instance, you may not be able to do much about factors such as more travel in highly litigious states or congested urban interstates, or cargo type and value. But ATRI said carriers still have opportunities to reduce exposure and improve pricing.

Fleets assuming more retained risk in their primary coverage layer generally saw lower overall insurance-related costs during the study period. That was true no matter the fleet size.

Fleets that reduced total purchased coverage experienced an average 2.4% reduction in combined liability losses and premium costs in the subsequent year, when adjusted for inflation.

ATRI suggested the savings likely came from both lower premiums and stronger fleet safety practices.

One of the most effective things a fleet can do to influence insurance costs is invest in a safety culture, safety technology, and training.

Which Safety Technologies Are Linked to Lower Truck Insurance Losses?

Many motor carriers are investing in safety technologies to support safer driving practices, improve insurance pricing, and offset increased exposure from lower insurance coverage levels.

ATRI asked survey respondents about their use of 12 safety technologies:

- Forward collision warning

- Lane departure warning

- Blind spot detection

- Adaptive cruise control

- Automated emergency braking

- Collision mitigation system

- Lane keeping assist

- Road-facing cameras

- Lane centering assist

- Active steering assist

- Driver-facing cameras

Between 2021 and 2024, deployment across all these technologies grew.

Forward collision warning increased the most, rising 24 percentage points in average deployment.

Lane departure warning and blind spot reduction also saw average deployment rates increase by over 20 percentage points.

On the other hand, driver-facing cameras had the lowest change in deployment rate, with their average deployment rate increasing by 8 percentage points. In fact, 5% of fleets decreased their use of driver-facing cameras over this period.

Every technology on the list, ATRI said, was used by at least one fleet with 25 trucks or fewer, a sign that safety technology is not just the province of large fleets.

Road-facing cameras were the most widely deployed technology, with an average rate of 70% in 2021 that grew to 87% in 2024.

ATRI said newer technologies such as lane-keeping assist and active steering assist are being adopted more slowly because they entered the market more recently.

The report found that six safety technologies had statistically significant correlations with lower per-mile liability losses: forward collision warning, lane departure warning, collision mitigation system, blind spot detection, adaptive cruise control, and automated emergency braking.

ATRI found that forward collision warning systems showed the strongest correlation with lower liability losses. The researchers noted that “failure to stop” remains one of the most common negligence claims in truck crash litigation.

More Details in the Report

The report, which can be downloaded on the ATRI website, also includes benchmarks on coverage levels, deductibles, self-insurance strategies, and captive insurance programs that fleets can use to compare their own risk-management approaches.

“Good fleets don’t just react passively to rate increases each year,” said Lynette Woodie, ArcBest manager of loss prevention and administration, in a news release. “They take the initiative by analyzing data and working closely with insurers to improve safety and reduce costs.”

Credit: Source link