Spot market rates continue to climb in the United States as fleets begin to once more struggle to land drivers amid a continued escalation of enforcement activities.

ACT Research defines the current recovery as being ‘supply-driven’ even as some capacity began returning to the market. Spot market rates set another all-time high, led by flatbed.

‘Supply-driven’ recovery continues

ACT Research says improving freight volumes in the for-hire market are being driven more by shrinking industry capacity than by a meaningful recovery in freight demand.

The latest ACT For-Hire Trucking Index showed the supply-demand balance tightened again in April as freight volumes remained elevated while capacity only slightly expanded. ACT’s seasonally adjusted Volume Index rose six points to 66.9, marking a new cycle high and continuing a trend that has seen the index remain above 60 in four of the past five months — a level not seen since late 2021.

Carter Vieth, research analyst at ACT Research, said the strengthening market is primarily supply-driven, with fewer trucks and drivers available to haul freight.

“As emphasized by the accelerating decline in the Driver Availability Index and the more chronic decline in the Capacity Index, this is largely a supply-driven recovery,” Vieth said.

The Capacity Index increased 1.9 points month over month to 50.2 in April from 48.1 in March, marking the first reading above the neutral 50 level in a year and only the third increase in the past three years. ACT said higher freight rates are beginning to encourage some fleets to add capacity again, though ongoing driver shortages and constrained equipment budgets remain significant hurdles.

Vieth noted recent increases in truck orders tied to upcoming EPA27 emissions regulations are beginning to support equipment purchases, although he expects most pre-buy activity to occur in the second half of 2026.

Despite the stronger freight environment, ACT warned the broader economic outlook remains uneven. Vieth said shippers may continue delaying inventory replenishment amid ongoing tariff uncertainty, even after a May 7 court ruling deemed the latest 10% Section 122 tariffs unlawful.

“The economy is likely to remain uneven, and effects on inflation and interest rates from the war in Iran curtail the demand outlook,” Vieth said. “But lower tariffs partly offset these effects. And capacity continues to exit the market, even with growing prebuy demand ahead of EPA27, largely as new FMCSA rules remove drivers.”

ACT’s Supply-Demand Balance Index climbed to 66.9 in April from 60.5 in March, reflecting stronger freight volumes even as capacity moved from contraction to modest expansion.

Flatbed rates continue to lead hot spot market

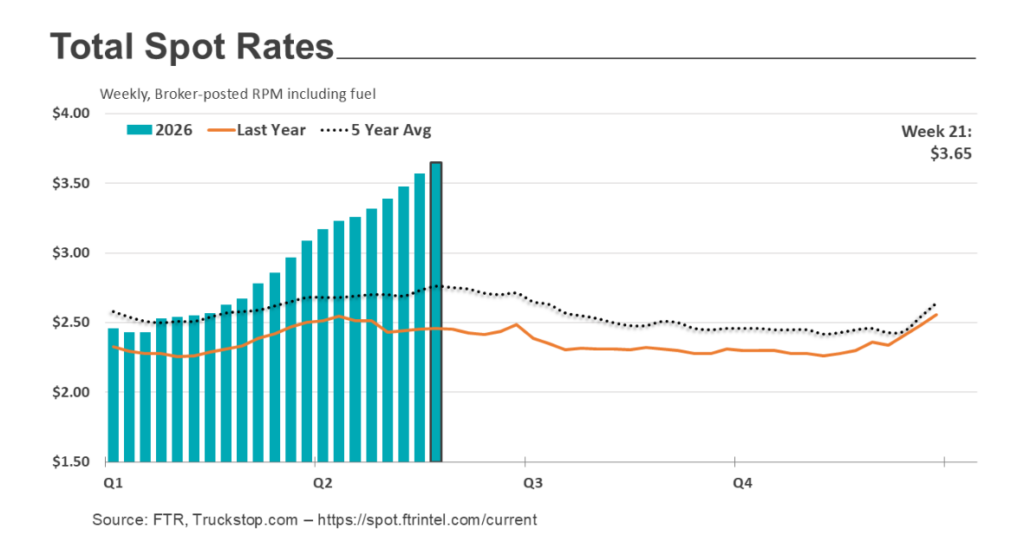

Spot market conditions continued to tighten in the week ended May 29, according to the latest data from Truckstop.com and FTR Transportation Intelligence, though the pace of tightening eased slightly from the volatility seen during International Roadcheck week.

Three of the four key market indicators declined week over week, led by a 15.1% drop in load availability. Truck availability also fell 11.5%, pushing the Market Demand Index (MDI) down 8.4 points to 200.7. Despite the lower MDI reading, market conditions remained substantially stronger than a year ago, with the index up 150.1% year over year.

Spot rates continued their upward march, climbing 2.2% to $3.65 per mile. Compared to the same week in 2025, spot rates were up 48.7%, underscoring the sharp tightening in available capacity that has developed this spring.

Total broker-posted spot rates set another all-time record during the week, as did flatbed spot rates. Dry van spot rates climbed to within three cents of the all-time high reached in the final week of 2021.

Flatbed freight remained particularly strong, with spot rates posting their largest week-over-week increase in eight weeks. Flatbed rates have now risen for 22 consecutive weeks and increased in 26 of the past 27 weeks, reflecting sustained demand in construction, manufacturing and industrial freight markets.

Refrigerated freight saw some moderation after an explosive run-up in recent weeks. Reefer spot rates fell slightly more than 10 cents per mile after surging nearly 74 cents over the previous four weeks — the largest four-week increase on record. Much of that increase was tied to the more than 52-cent spike recorded during International Roadcheck week, when enforcement activity temporarily sidelined additional capacity.

Meanwhile, national diesel prices eased eight cents to $5.51 per gallon from $5.59 the previous week, offering fleets a small reprieve from elevated operating costs.

Credit: Source link